April 9, 2013

Today marks the 71st anniversary of the Fall of Bataan, a National Holiday in the Philippines. On this day around 100,000 U.S. and Filipino soldiers laid down their arms and surrender to Gen. Yamashita.

Make the Philippines an American Battle Monument

April 9, 2013

Today marks the 71st anniversary of the Fall of Bataan, a National Holiday in the Philippines. On this day around 100,000 U.S. and Filipino soldiers laid down their arms and surrender to Gen. Yamashita.

March 16, 2013

Below is the WAIS post “Is the Euro Overvalued?” dated Feb. 28, 2010. It is my contention that the Euro, compared to the US dollar, is overvalued. Here’s why.

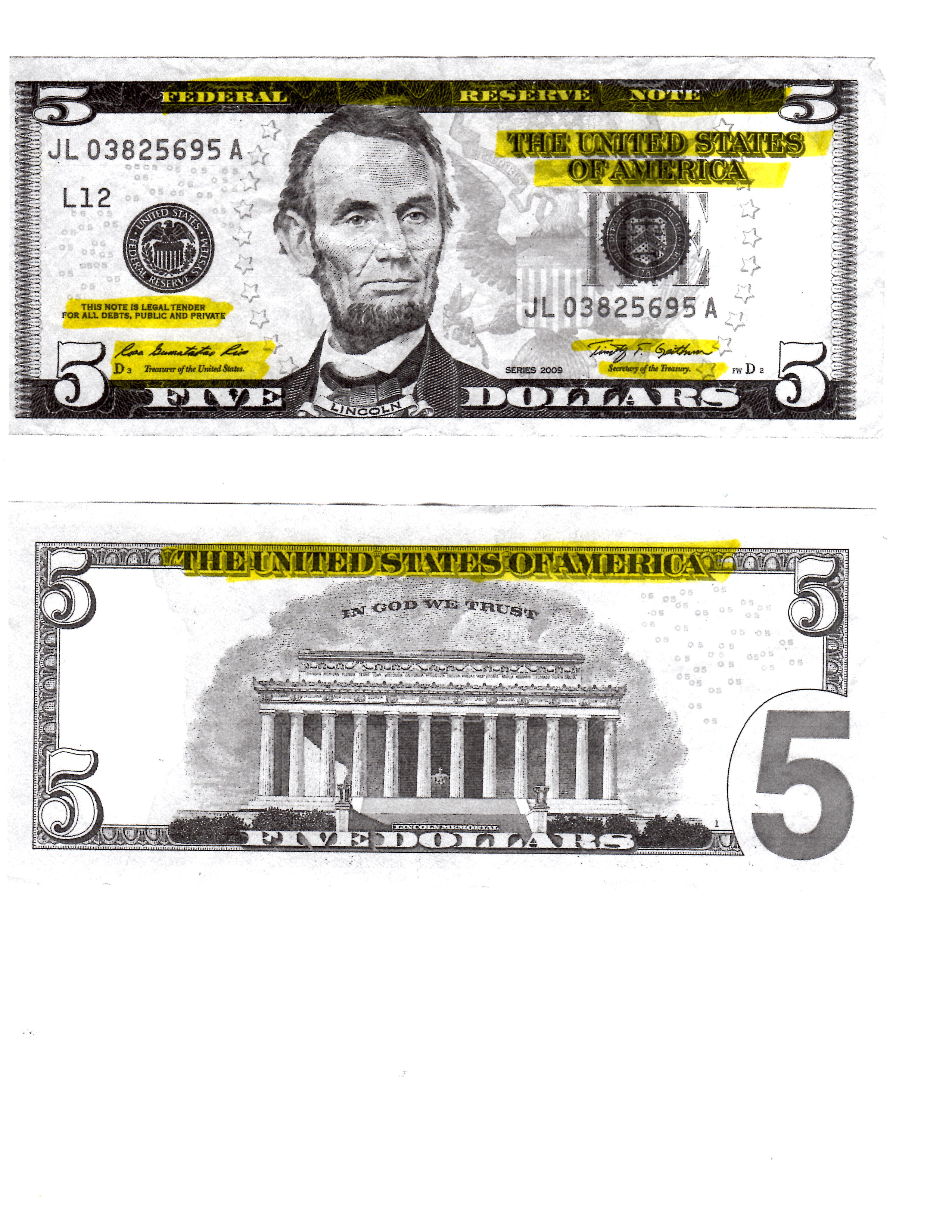

In every US dollar bill the words: “THIS NOTE IS LEGAL TENDER FOR ALL DEBTS PUBLIC AND PRIVATE” could be found. It is in fact a Federal Reserve (Bank) note, signed by the US Treasurer and the Secretary of the Treasury. On the back side of the note reads “THE UNITED STATES OF AMERICA” assures the holder in due course that every dollar bill is backed by the U.S. government.

Posted is an enlarge black & white copy of a US $5 bill. In yellow highlights are the features described above.

Next is the front and back specimen of a €5 bill. Where does it say there that Germany or the more prosperous members of the EU with stable economies will pay the holders of euros in due course? There is no saying what the EU-ECB will do or not do as in the case of the Cyprus bailout.

Granted that it is implied the note has the full backing and support of the EU, how long has the EU been around?

Why revisit this Feb. 2010 WAIS post now? It has something to do with: a.) The prediction that on March 15, 2013 the U.S. will officially be in recession. and b.) the ECB-IMF Cyprus bailout would involve US participation/contribution. It reminded me of the 1930’s collapse of the U.S. banking system. Yesterday’s much delayed bailout that is seen as a beginning of a new trend in bailouts where Cypriot bank depositors were asked to give up to 10% of their savings depending on their balances.

Could the ECB-IMF ask for technical assistance instead of funds from Washington DC? Continuous bailouts have limitations. Sometimes the cure could be worse than the disease.

See: Eurozone Debt Crisis Update: Cyprus’ Savers Suffer In Unprecedented bailout http://www.nedmacario.com/wp-admin/post.php?post=906&action=edit

Bienvenido Macario

Lemuria

Ancora Imparo

IGA

US FIVE DOLLAR BILL

March 16, 2013

As of March 15, 2013 here’s the news

By JUERGEN BAETZ | Associated Press – 18 hrs ago

http://news.yahoo.com/cyprus-secures-bailout-eurozone-imf-024409471–finance.html;_ylt=AwrNUbDd6URRKUoAMQzQtDMD

===================

This doesn’t say much. Again as in the second anniversary of the Fukushima triple disaster, I had to wait for a more realistic assessment of the news that at the same time would control if not prevent a bank run.

Highlights from news today on the Cyprus bailout: “Cyprus’ savers bear brunt of unprecedented bailout”

– The IMF will ask Washington DC to contribute to the bailout. Could the ECB-IMF ask Washington DC for technical assistance instead of funds?

– Spain is most likely next to require a bailout. This means a bank run on Monday is likely.

– Electronic transfers of funds over the weekend have been prevent by Cyprus since over 50% are non-residents.

=====================

I think a news about a recession would have been better than this type of bailout. Bank runs like the ones seen in May 2012 in Spain and Greece could happen again.

I’ll fix this post later.

Bienvenido Macario

Lemuria

Ancora Imparo

IGA

Reuters – 1 hr 1 min ago Saturday, March 16, 2013

http://news.yahoo.com/savers-forced-bear-costs-cyprus-bailout-051941784.html;_ylt=AwrNUbDd6URRKUoAHQzQtDMD

Reuters/Reuters – People gather at an automatic teller machine in Nicosia March 16, 2013. REUTERS/Yiannis Nisiotis

By Annika Breidthardt and Robin Emmott and Michele Kambas

BRUSSELS/NICOSIA (Reuters) – The euro zone agreed on Saturday to hand Cyprus a bailout worth 10 billion euros ($13 billion), but demanded depositors in its banks forfeit some money to stave off bankruptcy despite the risk of a wider run on savings.

The eastern Mediterranean island becomes the fifth country after Greece, Ireland, Portugal and Spain to turn to the euro zone for financial help during the region’s debt crisis.

In a radical departure from previous aid packages – and one that gave rise to incredulity and anger across the country – euro zone finance ministers forced Cyprus’ savers to pay up to 10 percent of their deposits to raise almost 6 billion euros.

Parliament was due to meet on Sunday to vote on the measure, and approval was far from assured.

The decision prompted a run on cashpoints, most of which were depleted by mid afternoon, and co-operative credit societies closed to prevent angry savers withdrawing deposits.

Almost half Cyprus’s bank depositors are believed to be non-resident Russians, but most queuing on Saturday at automatic teller machines appeared to be Cypriots.

President Nicos Anastasiades, elected three weeks ago with a pledge to negotiate a swift bailout, said refusal to agree to terms would have led to the collapse of the two largest banks.

“On Tuesday … We would either choose the catastrophic scenario of disorderly bankruptcy or the scenario of a painful but controlled management of the crisis,” Anastasiades said in written statement.

In several statements since his election, he had previously categorically ruled out a deposit haircut.

“My initial reaction is one of shock,” said Nicholas Papadopoulos, head of parliament’s financial affairs committee. “This decision is much worse than what we expected and contrary to what the government was assuring us, right up until last night,” he told Reuters, without saying whether he would back the measure or whether he thought it would pass.

Papadopoulos is vice-chairman of the Democratic Party, a partner in Cyprus’s centre-right ruling coalition and whose support in parliament will be crucial to pass any haircut.

Parliament was expected to convene from 1600 local (1400 GMT) on Sunday to discuss the emergency legislation. Without parliamentary approval, a haircut cannot take place.

‘THEFT, PURE AND SIMPLE’

The bailout was smaller than initially expected and is mainly needed to recapitalize Cypriot banksthat were hit by a sovereign debt restructuring in Greece.

The deposit levy – set at 9.9 percent on bank deposits exceeding 100,000 euros and 6.7 percent on anything below that – will take place on Tuesday after a bank holiday on Monday.

To guard against capital flight, Cyprus took immediate steps to prevent electronic money transfers over the weekend.

At one cashpoint in the capital Nicosia, a pensioner couple said they had visited several automatic teller machines without success. “We are trying to pull as much as we can,” one told Reuters, reaching for a wallet containing four debit cards.

“I’m extremely angry. I worked years and years to get it together and now I am losing it on the say-so of the Dutch and the Germans,” said British-Cypriot Andy Georgiou, 54, who returned to Cyprus in mid-2012 with his savings.

“They call Sicily the island of the mafia. It’s not Sicily, it’s Cyprus. This is theft, pure and simple,” said a pensioner.

The levy breaks a euro zone taboo by hitting depositors.

It prompted Spain, considered the next most likely state to seek a sovereign rescue though supported recently by a European Central Bank promise to buy government debt if necessary, to deny savers in other countries risked being similarly penalized.

The bailout was specific to Cyprus and its bloated banking sector and “could not be extrapolated to any other country,” an economy ministry source in Madrid said.

In Brussels, Dutch Finance Minister Jeroen Dijsselbloem said it would not otherwise have been possible to save Cyprus’s financial sector which, compared with national economic output, is more than twice as big as the EU average.

“As it is a contribution to the financial stability of Cyprus, it seems just to ask for a contribution of all deposit holders,” Dijsselbloem, who chaired the ministerial meeting, told reporters.

The island’s bailout had repeatedly been delayed amid concerns from other EU states that its close business relations with Russia, and a banking system flush with Russian cash, made it a conduit for money-laundering.

In return for emergency loans, Cyprus agreed to increase its corporate tax rate by 2.5 percentage points to 12.5 percent. This should boost revenues, limiting the size of the loan needed from the euro zone and keep down public debt.

RUSSIAN AID

International Monetary Fund Managing Director Christine Lagarde, who attended the Brussels meeting, said she backed the deal and would ask the IMF board in Washington to contribute.

“We believe the proposal is sustainable for the Cyprus economy,” she said. “The IMF is considering proposing a contribution to the financing of the package … The exact amount is not yet specified.”

Cyprus, with a gross domestic product of barely 0.2 percent of the bloc’s overall output, applied for aid last June. But negotiations became bogged down.

Moscow, with close ties to Nicosia, will also likely extend a 2.5 billion euro loan by five years to 2021 at a lower cost.

“My understanding is that the Russian government is ready to make (such) a contribution,” said the EU’s top economic official, Olli Rehn.

Cyprus originally estimated it needed 17 billion euros – almost its annual output – to restore its economy to health.

But because a loan of that magnitude would call into question its ability ever to pay it back, policymakers sought more revenue sources in Cyprus itself.

The Greek units of Cypriot banks were excluded from the deposit levy, Greek finance minister Yiannis Stournaras said.

(Additional reporting by Julien Ponthus Harry Papachristou; Writing by Robin Emmott, John O’Donnell and Michele Kambas; Editing by Jason Webb)